Tenth CREMMA school

The Laboratory of Mathematical Modelling and Numeric in Engineering Sciences (LAMSIN) of Tunis El Manar University, Institut du Risque et de l'Assurance of Le Mans University, CMAP-Ecole Polytechnique (Palaiseau, France), ESPRIT and The Mediterranean Institute for the Mathematical Sciences (MIMS) organize the tenth spring school of the Euro-Mediteranean Research Center for Mathematics and its Applications (CREMMA).

The location will be in Tunisia.

The school will take place at Tunis National School of Administration (ENA), 24 Rue Dr Calmette, Tunis 1082, from 6 until 10 April, 2020. The lectures are devoted to recent advances in Stochastic Modeling and Applications in Insurance and Finance. This year's theme is "Stochastic control, machine learning and Applications in Finance and Insurance". The aim of this meeting is to bring together researchers in some of the most active and promising areas of research of stochastic control and games. The program of the conference will consist of three courses. It also contains a half-day whorkshop dedicated to recent results related to the spring school theme.

Lectures

Langevin dynamics and non convex optimization

Measure derivative and the Ito calculus

Mean-field Langevin dynamics and neural networks

Registration

The conference fees are as follows

Accomodation

Scientific commitee

- Anis Matoussi:anis.matoussi@univ-lemans.fr Organization commitee

- Anis Matoussi:anis.matoussi@univ-lemans.fr The School is sponsored by :

- Zhenjie REN (Paris Dauphine University, France)

Mean-field Langevin Dynamics and Neural Networks

- Wissal SABBAGH (ENSAE-CREST, France)

Conterparty credit risk and XVA : Methodology and implementation

- Chao ZHOU (National University of Singapore)

Deep learning based methods in mathematical finance and insurance

For any question concerning the lectures, contact the program committee:

Anis Matoussi, Professor, le Mans University, anis.matoussi@univ-lemans.fr,

Mohamed Mnif, Professor, ENIT, University Tunis El Manar, mohamed.mnif@enit.rnu.tn.

Abstracts :

- Zhenjie REN (Paris Dauphine University, France) : Mean-field Langevin Dynamics and Neural Networks

Abstract:In recent years the neural networks become a popular and powerful tool in applications such as image classification, natural language processing, automatic driving, computer games and so on. Mathematically, it is an overparametrized non convex optimization problem. How such problem can efficiently solved by simple gradient descent algorithm is still mysterious. In this course, we propose a mathematic model, the so-called Mean-Field Langevin Dynamics to study the solvability of the gradient decent algorithm for neural networks. The basic contents include:

- Wissal SABBAGH (ENSAE-CREST, France): Conterparty credit risk and XVA : Methodology and implementation

Abstract:Before the financial crisis of 2007-2008, the standard approaches to pricing and fair value measurement of portfolios and trading books were based on the assumption of risk-free counterparties and rates. However, the crisis highlighted the importance of counterparty risk and showed that pricing approaches should be revised. In fact, the losses due to the deterioration in the creditworthiness of a counterparty during the financial crisis exceeded the losses arising from actual defaults, according to the Basel Committee on Banking Supervision (BCBS). Therefore, the regulators gradually introduced new valuation adjustments in order to take into account the effects of credit, funding and capital costs and, as a consequence, the pricing of derivatives has become more and more complicated. These adjustments, named X Value Adjustments (XVA), are considered today among the main Profit & Losses centers of investment banks, and they affect many areas such as modeling, pricing, risk management, regulation. In this lecture, we present the mathematical structure of these adjustments and develop some numerical schemes to approximate the XVA equations.

- Chao ZHOU (National University of Singapore): Deep learning based methods in mathematical finance and insurance

Abstract:In this lecture, we introduce some recently developed Deep Learning based numerical methods for problems in Mathematical Finance and Insurance, notably in the high-dimensional cases. Students will have a hand-on experience in numerically solving problems with Python or other programming languages.

The application must include:

- a detailed academic CV (specific and detailed programs, evaluation),

- a cover letter with the subject of the thesis organization and some details of the results already

obtained,

- supervisor's recommendation letter.

All the candidacies have to be sent to Chefia Ziri :chefia.ziri@enit.utm.tn and will be considered by the program committee.

Deadline for registration: March 2, 2020.

- Regular registration: 150 euros

- From Maghreb countries registration: 50 euros

- From Tunisia registration 150 DT.

Payment of registration fees can be made with purchase orders ("Bons de Commande") from

research laboratories, academic or business institutions only for Tunisian participants or

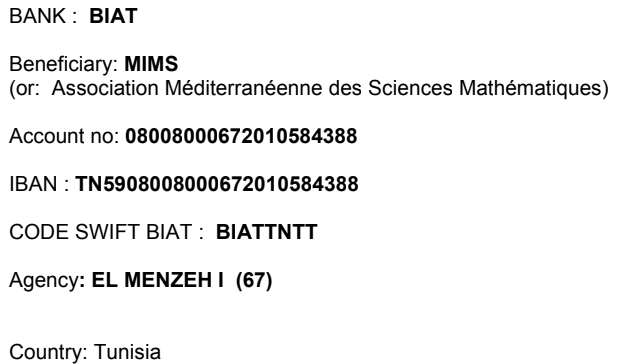

by transfer to the following MIMS bank account for the other participants:

Cancellation policy: Please note that we cannot refund registration fees.

The conference fee covers:

- Lunches on every day of the conference (i.e. Monday-Friday)

- Coffee breaks

- Hotel Belvédère Fourati, you can walk ( 30 minutes), 10 Avenue Des Etats Unis D'Amerique,

Tunis 1002, http://belvedere-fourati.tunis-hotels-tn.com/en/

- Hotel Ariha, you can walk ( 20 minutes), 110 Rue de La Palestine, Tunis 1002,http://www.hotelariha.com/english/

- Mohamed Mnif:mohamed.mnif@enit.rnu.tn

- Habib Ouerdiane:habib.ouerdiane@fst.rnu.tn

- Nizar Touzi:nizar.touzi@polytechnique.edu

- Mohamed Mnif:mohamed.mnif@enit.rnu.tn

- Chefia Ziri:chefia.ziri@enit.utm.tn

- Lamia Ben Ajmia:lamiabenajmia01@gmail.com

- Mohamed Anis Ben Lasmar:mohamedanis.benlasmar@esprit.tn

- CMAP-Ecole Polytechniques, Palaiseau-France : Chair Risques Financiers of Risk foundation (Institut Louis Bachelier) & CMAP-Ecole Polytechniques, Palaiseau-France .

- Institut du Risque et de l'Assurance & Laboratoire Manceaux de Mathématiques (LMM) : Chair Risques Emergents ou Atypiques en Assurance (RE2A) of Risk foundation (Institut Louis Bachelier), Le Mans University, MMA-COVEA & CMAP-Ecole Polytechniques .

- ESPRIT.

- Université Tunis El Manar : LAMSIN.

|

|

|

|

|